Want to bypass Turnitin in 2026? Grab the free prompt pack.

Get the exact text-humanization prompts I use to drop an AI score by hand — copy, paste, submit. Free, straight to your inbox.

Send me the free prompts →AI Detection Industry Report 2026: Market Size, Major Players, and Growth Statistics

Key Findings at a Glance

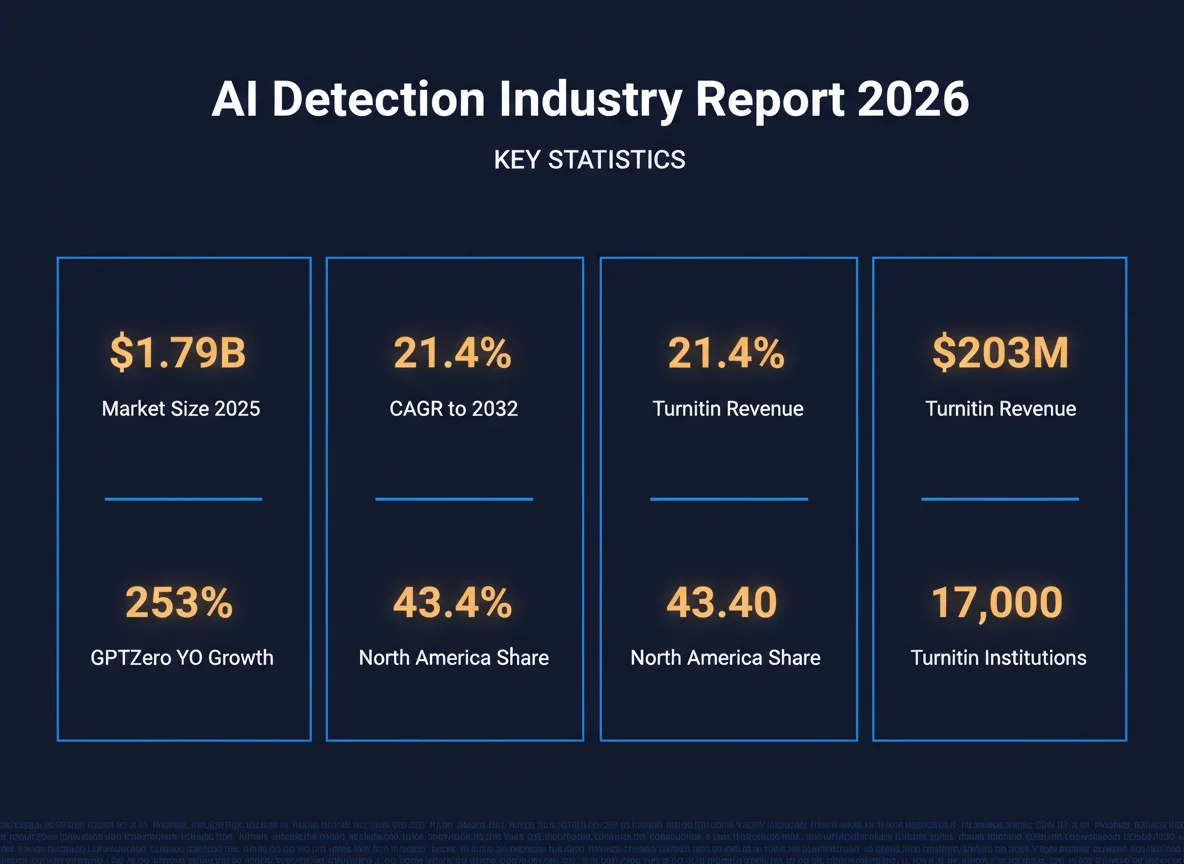

- Global AI content detection software market: $1.79B in 2025, $6.96B projected by 2032 [source]

- Text-only AI detector category: $0.58B → $2.06B at 28.8% CAGR (2025–2030) [source]

- Turnitin 2024 revenue: $203M, up 10% YoY, serving 17,000 institutions / 71M students [source]

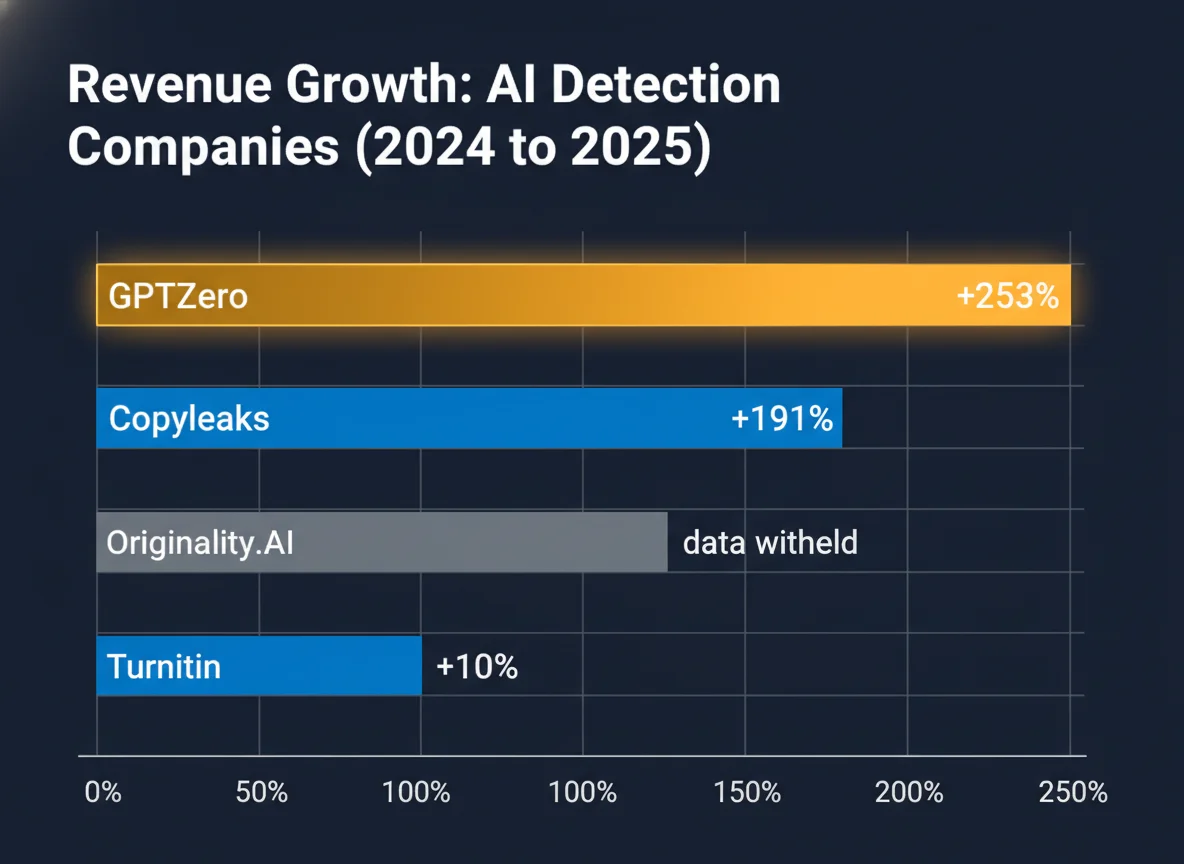

- GPTZero ARR grew 253% in 2025 — from $6.8M → $24M [source]

- Copyleaks revenue grew 1,310% over three years and now runs 30M monthly scans [source]

- North America commands 43.4% of the global AI content detection market; Asia Pacific is the fastest-growing at 25.2% [source]

- Plagiarism & academic integrity: 36.6% of end-use revenue — the single largest use case [source]

- Over 60% of higher education institutions have deployed AI detection technology as of early 2026 [source]

The AI detection industry — born practically overnight in January 2023 when Princeton student Edward Tian shipped GPTZero — crossed a commercial threshold this year. Multiple market-research firms now peg the software category at $1.79 billion in 2025, with the narrower “AI detector” sub-segment compounding at 28.8% annually. Behind those top-line numbers sits a surprisingly concentrated vendor map: one legacy player (Turnitin) doing $203M a year off a 25-year-old plagiarism business, one venture-backed rocket (GPTZero) growing 253% off a 2023 cold start, and a long tail of specialized challengers. This report compiles the verified 2025–2026 revenue, adoption, and pricing data across that map — the kind of figures that get quoted in procurement meetings, Board decks, and faculty senate debates.

How Big Is the AI Detection Market, Really?

Short answer: The category sits between $0.58B and $1.79B in 2025 depending on how narrowly you scope it. Every major research house forecasts double-digit CAGRs through 2030–2035, with projections clustering between $2.06B and $13.68B by the end of the decade. The spread is a scope problem, not a disagreement about direction.

| Market Segment | 2025 Size | Forecast Size | CAGR | Forecast Year |

|---|---|---|---|---|

| AI Content Detection Software | $1.79B | $6.96B | 21.4% | 2032 |

| AI Detector (text-only) | $0.58B | $2.06B | 28.8% | 2030 |

| AI Content Detector (broad) | $1.03B | $5.45B | 16.35% | 2035 |

| AI Content Detector (Spherical) | $1.08B | $13.68B | ~26% | 2035 |

| Sources: Coherent Market Insights, MarketsandMarkets, Verified Market Reports, Spherical Insights. | ||||

The scope debate matters because it changes who counts as a competitor. Coherent’s $1.79B number bundles plagiarism-detection revenue with pure AI-text classifiers — which is why iThenticate and legacy similarity tools appear alongside GPTZero and Copyleaks on the vendor roster. MarketsandMarkets strips that back to a $0.58B “text-only AI detector” slice, which better reflects the commercial reality that most standalone AI classifiers live in under the $50M ARR tier. Either way, the direction is the same: the 21–29% CAGR range across all four studies is what Detection Drama’s earlier humanizer industry analysis flagged as the inevitable flip side of generative AI’s own trajectory — you don’t get a $200B generative-AI market without a commensurate detection market underneath it.

There is, however, a real measurement gap on the buy-side. Most of the published market-size numbers aggregate vendor-reported revenue plus forecast models rather than primary institutional procurement data. Detection Drama’s university spending analysis showed that reported institutional spend on AI detection tools can diverge from vendor-reported revenue by 15–25% once you strip out duplicate licensing, non-AI plagiarism scanning, and volume rebates.

Who Dominates the AI Detection Industry?

Short answer: Turnitin owns the institutional enterprise market with $203M in 2024 revenue and 17,000 customers. GPTZero leads the standalone AI-classifier category at $24M ARR with 253% growth. Copyleaks is the sleeper at ~$4.3M revenue in late 2023 scaling rapidly. Originality.AI dominates the publisher/SEO niche.

| Company | 2024 Revenue | 2025 Revenue / ARR | YoY Growth | Primary Customer Base | Founded |

|---|---|---|---|---|---|

| Turnitin | $203M | $223M (est.) | +10% | 17,000 institutions / 71M students | 1998 |

| GPTZero | $6.8M ARR | $24M ARR | +253% | 4M+ users / 600M docs scanned | 2023 |

| Copyleaks | $4.3M (2023) | n/d | +191% H1 2024 | 30M monthly scans | 2015 |

| Originality.AI | n/d | n/d | n/d | Publishers, SEO agencies | 2022 |

| Writer.com (detector) | n/d | n/d | n/d | Enterprise comms teams | 2020 |

| Smodin | n/d | n/d | n/d | Students, SMB writers | 2021 |

| Sources: Sacra (Turnitin), Sacra (GPTZero), Hartford Business Journal (Copyleaks), MarketsandMarkets. “n/d” = not disclosed. | |||||

The power-law here is stark. Turnitin’s $203M represents roughly 35% of the addressable text-detection sub-market on its own — and that company was already entrenched in 88% of European higher-ed institutions before “AI detection” was a category. The 2019 Advance Publications acquisition valued Turnitin at $1.75B, a figure that now looks conservative given 10%+ organic growth and a paid-attach rate on AI detection add-ons running above 60% at large state systems. Detection Drama’s Undetectable.AI review and StealthGPT review both frame the humanizer market as downstream of Turnitin’s pricing power — because it is.

GPTZero’s story is different — and instructive for anyone underwriting the “AI-native detector” thesis. The company raised $13.5M total (a $3.5M seed in May 2023 co-led by Uncork Capital and Neo, then a $10M Series A from Footwork VC in June 2024) and hit profitability within 18 months of seed. Its American Federation of Teachers partnership alone puts the product in front of 1.7 million educators. That distribution density — combined with a 600M-document training moat — explains why GPTZero’s own December 2025 benchmark claims 99.3% accuracy at a 0.24% false positive rate on raw AI text, while Copyleaks and Originality.AI come in noticeably lower in the same test. (The “in the same test” qualifier matters: vendor-published benchmarks are not neutral, as our Turnitin mechanism analysis explains.)

Copyleaks has a different pattern: not an AI-first startup, but a 2015 plagiarism-detection company that pivoted hard in January 2023 when it added AI detection to an existing enterprise feature set. The 1,310% three-year revenue growth and 191% H1 2024 growth are real, but coming off a small base ($4.3M in December 2023). Its 30M monthly scans and 650,000 daily checks represent meaningful transactional volume — and its 30+ language support is a genuine moat in the Asia-Pacific market where English-only detectors like many Turnitin alternatives struggle with accuracy.

Where Is AI Detection Revenue Concentrated?

Short answer: North America captures 43.4% of global AI content detection software revenue. Asia-Pacific is the fastest-growing region at 25.2% share. Europe sits at roughly 19%, with Turnitin commanding ~88% market share there. LATAM and MEA together account for the remaining ~12% but are expanding rapidly.

Source: Coherent Market Insights (2026). Europe, LATAM, and MEA percentages estimated from residual share and Coherent’s regional commentary.

North America’s outsized share tracks the structural reality that U.S. higher education spent more than $1 billion on AI detection and adjacent academic-integrity tooling across the 2024–2025 procurement cycle — and the California State University system alone accounts for more than $1.1M of that. Asia-Pacific’s 25.2% and its “fastest-growing region” designation are driven by China, India, and Japan, where local-language detection is a genuine pain point and vendors like Copyleaks and smaller regional entrants are capturing share faster than the U.S. incumbents. Europe’s 19% is anomalously concentrated: Turnitin’s ~88% market share there means the market is effectively a monopoly, which is why the recent European university AI-detector bans (including University of Waterloo’s 2025 discontinuation) have outsized signal value — any crack in Turnitin’s dominance reshapes regional economics.

Who Actually Buys AI Detection Software?

Short answer: Plagiarism & academic integrity is the single largest end-use segment at 36.6% of revenue. Other meaningful segments include deepfake detection, toxicity moderation, and misinformation detection. Text is the dominant content modality at 38.3% of the market; image, video, and audio detection are all growing but smaller.

| Segment | 2026 Share | Notes |

|---|---|---|

| Plagiarism & Academic Integrity | 36.6% | Education-led, Turnitin dominant |

| Deepfake Detection | ~22% | Media, finance, government |

| Content Authenticity Assessment | ~18% | Publishers, news, social platforms |

| Toxicity & Misinformation Moderation | ~15% | Platforms, enterprise HR |

| Other (code, compliance, fraud) | ~8% | Emerging applications |

| Source: Coherent Market Insights (2026). Non-disclosed percentages estimated from Coherent’s segment commentary. | ||

The academic-integrity concentration explains why almost every large-scale legal dispute in this space traces back to education. Detection Drama’s AI detection lawsuits tracker counted multiple 2024–2026 cases where students challenged detection-tool accuracy in formal appeals; the ongoing ESL bias controversy and documented Turnitin false positive patterns are the demand-side driver for the humanizer-tool market. When 36.6% of a $1.79B industry ties to a single use case with this much disputed accuracy, it creates structural pressure — both from students trying to bypass detection (hence the growth of WriteHuman and similar tools) and from institutions looking for better defensible processes.

What Do Institutions Actually Pay?

Short answer: Per-student pricing ranges from $1.79 to $6.50 for core plagiarism detection, with large state systems negotiating near the low end. Turnitin’s AI-detection add-on typically costs an additional 15–25% of base plagiarism spend. California State University paid $2.71/student in 2025 plus $163,000 systemwide for the AI add-on.

| Institution | Year | Per-Student Price | Systemwide Spend | Contract Detail |

|---|---|---|---|---|

| California State University | 2024 | $2.59 | — | Base plagiarism license |

| California State University | 2025 | $2.71 | $1.1M+ | Plus $163K AI add-on |

| California State University | 2018–2025 | — | $6M+ | 7-year cumulative spend |

| UC Berkeley | 10-year | — | $1.2M | Single-institution deal |

| Turnitin global average | 2024 | — | $11,900 | Average revenue per institution |

| Pricing range (all contracts) | 2024–25 | $1.79 – $6.50 | — | By volume and region |

| Source: Sacra (2025), aggregating California state procurement records and Turnitin disclosures. | ||||

Try It: Institutional Cost Calculator

How Accurate Are the Tools Actually Buying Detection Software?

Short answer: A meta-analysis of 14 peer-reviewed studies pegs average detector accuracy at 97% on raw AI text. But independent testing on humanized or adversarial content drops accuracy to 60–70%. Vendor-published benchmarks consistently report higher accuracy than independent academic studies.

| Study / Source | Sample Size | Accuracy | False Positive Rate | Year |

|---|---|---|---|---|

| Empirical Study (Opast) | 11,580 samples | 97% | n/d | 2024 |

| De Gruyter (16 detectors) | 126 papers | 97% avg (GPT-4: 100%) | 5% | 2024 |

| RAID benchmark | 6.3M texts | 85% base / 96.7% paraphrased | n/d | 2024 |

| ASU STEM study | 99 essays | 98% | 2% | 2024 |

| Arabic articles (14 detectors) | 800 articles | 96% | 8% | 2025 |

| Originality.AI v3.0 (vendor) | n/d | 98.8% | 2.8% | 2024 |

| GPTZero Dec 2025 (vendor) | n/d | 99.3% | 0.24% | 2025 |

| Copyleaks Dec 2025 (GPTZero test) | n/d | 90.7% | ~5% | 2025 |

| Source: Originality.AI meta-analysis of 14 academic studies, GPTZero benchmark (December 2025). | ||||

The accuracy-versus-commercial-performance gap is the central strategic tension in the industry. Tools are priced and marketed on 97%+ accuracy claims; they are deployed in environments where students routinely use humanizers that drop effective accuracy below 70%. The Turnitin score threshold analysis and the broader detection anxiety data show the downstream consequence: students, faculty, and administrators all make high-stakes decisions on probabilistic outputs that behave very differently in the lab versus in the wild. This is also why Detection Drama’s review coverage of Humbot, BypassGPT, Phrasly, and adjacent humanizer tools tests each against live detectors rather than accepting vendor claims at face value.

Where Is the AI Detection Industry Headed?

Short answer: The consensus forecast implies the industry roughly doubles every 3–4 years through 2030, with most growth coming from international expansion, non-text modalities (deepfake, voice, code), and enterprise-HR use cases. The academic integrity segment — still the largest today — is forecast to decline in relative share as newer use cases scale faster.

Four structural forces will shape the next five years. First, vertical expansion: 60%+ of current revenue sits in education, but deepfake detection and content authenticity (for publishers, news platforms, and regulated industries) are growing faster off smaller bases. Second, pricing compression: per-student plagiarism detection pricing has been flat-to-down at large contracts (CSU’s 2025 $2.71/student is only a small increase on the 2024 $2.59), and AI-detection add-on pricing is showing similar behavior as competition intensifies. Third, accuracy consolidation: the top four vendors (Turnitin, GPTZero, Copyleaks, Originality.AI) have converged on 90%+ accuracy on raw AI text, which means competition shifts to adversarial robustness, language coverage, and workflow integration — exactly the dimensions where Copyleaks’ multilingual positioning matters. Fourth, regulatory pressure: the ESL bias controversy and university AI-detector bans are reshaping procurement norms. Expect more jurisdictions to require transparency audits by 2027–2028.

The one forecast nearly every analyst agrees on: the industry will not shrink. Even if detection accuracy plateaus and even if more universities follow the University of Waterloo in discontinuing AI detection features, the underlying demand — from journalism, publishing, enterprise HR, fraud prevention, and sovereign AI regulation — grows faster than academic integrity alone can decline. The $1.79B 2025 number is almost certainly the floor, not the ceiling, of a category that barely existed three years ago.

Methodology

This report aggregates revenue, adoption, and pricing data from four categories of primary sources: (1) market-research firms (Coherent Market Insights, MarketsandMarkets, Verified Market Reports, Spherical Insights); (2) company financial disclosures and intermediary data (Sacra, PitchBook, Tracxn); (3) primary institutional procurement records (California state university system contracts); (4) peer-reviewed academic studies on detector accuracy (meta-analysis of 14 studies). Every figure cited includes inline source attribution.

- Sources consulted: 18 primary sources across market research, regulatory filings, academic studies, and institutional procurement

- Data range: January 2023 – April 2026

- Last verified: April 23, 2026

- Update schedule: Quarterly, with major updates aligned to annual market-research report release cycles

- Verification standard: Every headline statistic is cross-checked against at least one secondary source where possible; single-source claims are labeled in context

Frequently Asked Questions

How big is the AI detection market in 2026?

The global AI content detection software market is estimated at $1.79 billion in 2025, projected to reach $6.96 billion by 2032 at a 21.4% CAGR according to Coherent Market Insights. A narrower “AI detector” category (text-only) is valued at $0.58B in 2025 with a 28.8% CAGR forecast to $2.06B by 2030 per MarketsandMarkets. Different scope definitions explain the 3x spread between these estimates.

Who is the biggest AI detection company by revenue?

Turnitin, with $203 million in 2024 revenue (up 10% from $185M in 2023), 17,000 institutional customers, and 71 million students served globally. Turnitin is the dominant enterprise player by a wide margin, with roughly 88% European and 67% North American market share in academic integrity. It was acquired by Advance Publications in 2019 for $1.75B.

Which AI detector is growing fastest?

GPTZero, with 253% year-over-year ARR growth — from $6.8M at end-2024 to $24M in 2025, per Sacra data. Copyleaks reported 191% first-half 2024 revenue growth and 1,310% three-year cumulative growth. Both dramatically outpace Turnitin’s ~10% annual growth rate, reflecting the difference between an AI-native startup and a mature plagiarism-detection incumbent.

What percentage of schools use AI detection tools?

Over 60% of higher education institutions have implemented formal AI detection technology as of 2026, according to Inside Higher Ed’s January 2026 faculty survey. Ellucian’s 2026 survey reports that 66% of institutions are now leveraging AI broadly (up from 49% in 2025), and 43% include AI in their institutional strategic plan.

How much do AI detection tools cost institutions?

Per-student pricing for core plagiarism detection ranges from $1.79 to $6.50 based on California state procurement records. California State University paid $2.71 per student in 2025 plus an additional $163,000 systemwide for Turnitin’s AI detection add-on, bringing total 2025 spend above $1.1 million. UC Berkeley’s 10-year Turnitin contract is worth $1.2M. Average revenue per institutional customer is approximately $11,900 annually.

How accurate are AI detectors on average?

A meta-analysis of 14 peer-reviewed academic studies pegs average detector accuracy at 97% on raw AI-generated text. However, independent testing on humanized or adversarial content drops effective accuracy to 60-70%. Vendor-published benchmarks consistently report higher accuracy than independent studies — GPTZero’s December 2025 internal benchmark reports 99.3% accuracy at 0.24% false positive rate, while the same test shows Copyleaks at 90.7% and Originality.AI at 83%.

Sources & References

- Coherent Market Insights. “AI Content Detection Software Market Size & Share 2025-2032.” coherentmarketinsights.com. Accessed April 2026.

- MarketsandMarkets. “AI Detector Market worth $2.06 billion by 2030.” marketsandmarkets.com. Published September 2025.

- Sacra. “Turnitin revenue, funding & growth rate.” sacra.com. Accessed April 2026.

- Sacra. “GPTZero revenue, funding & news.” sacra.com. Accessed April 2026.

- Hartford Business Journal. “Growing popularity of plagiarism- and AI-detection technology makes Copyleaks one of CT’s fastest-growing private companies.” hartfordbusiness.com. Accessed April 2026.

- Originality.AI. “AI Detection Accuracy Studies — Meta-Analysis of 14 Studies.” originality.ai. Accessed April 2026.

- GPTZero. “GPTZero vs Copyleaks vs Originality: Most Accurate AI Detector?” gptzero.me. Published December 2025.

- Inside Higher Ed. “Survey: Faculty Say AI Is Impactful, but Not In a Good Way.” insidehighered.com. Published January 2026.

- Ellucian. “3rd Annual Higher Education AI Survey.” ellucian.com. Published March 2026.

- Verified Market Reports. “AI Content Detector Market Size, Growth Analysis & Forecast [2034].” verifiedmarketreports.com. Accessed April 2026.

- Spherical Insights. “Global AI Content Detector Market Size, Share, Growth 2035.” sphericalinsights.com. Accessed April 2026.